ACCA(FA)高頻考點詳解,discount的會計處理

發布日期:2022-09-28 09:06:35

在ACCA考試中,折扣知識點可是FA科目非常重要的一個內容,本文會通過例題的形式幫助大家理解和掌握discount的會計處理和計算。

01、Definitions

Trade discount(商業折扣)

A trade discount is a reduction in the list price. It is often given in return for bulk purchase order.

在采購或者是銷售的時候就已經確定了是否會使用折扣

Settlement discount (現金折扣)

A settlement discount (cash discount) is a reduction of in the amount payable. It is often given in return for earlier payment.

在采購或者是銷售發生的時候是不確定的,在付款日才確定是否會使用折扣。

02、Accounting for discount

Trade discount 商業折扣

Trade discounts allowed should be deducted from the sales price.:直接在采購或者銷售的時候就減去

Purchase站在采購方的角度

Golden purchases goods on credit from Supplier A at a gross cost of $100, and receives a trade discount of 5%.

Dr Purchase 95 (100-100*5%)

Cr Payable 95 (100-100*5%)

Sale 站在銷售方的角度

Golden purchases goods on credit from Customer B at a gross cost of $100, and offer a trade discount of 5%.

Dr Receivables 95 (100-100*5%)

Cr Sales 95 (100-100*5%)

cash discount 現金折扣

現金折扣的處理分為discount received和 discount allowed:

For buyer (discount received):

At transaction date, record full invoiced amount. If subsequently take the discount, then the discount received is recorded as an income.

站在采購方的角度,如果后續使用了現金折扣,那么就記錄一個收入discount received。

For seller (discount allowed):

If a customer is expected to take up a cash/settlement discount, the discount is deducted from sales revenue. If the customer subsequently does not take up the discount, the discount is then recorded as sales revenue.

站在買方的角度,處理較為復雜;首先在發生銷售時,如果企業預計客戶會接受現金折扣),則在記錄銷售時應確認收入減去此折扣。

If the customer is not expected to take up the discount, the full invoiced amount is recognized as revenue when recording the sale.

如果在發生銷售的時候,預計客戶不會使用現金折扣,那么就記錄銷售的時候就按照實際銷售的金額全額記錄。

If the customer subsequently does take up the discount, revenue is then reduced by the discount.

如果客戶后續使用了這個折扣,那么就要調整收入,從收入中將折扣減去。

看定義對于同學們來說,還是非常容易混淆,所以接下來我們會通過一道例題,給大家展示不同情況下的會計處理和計算。

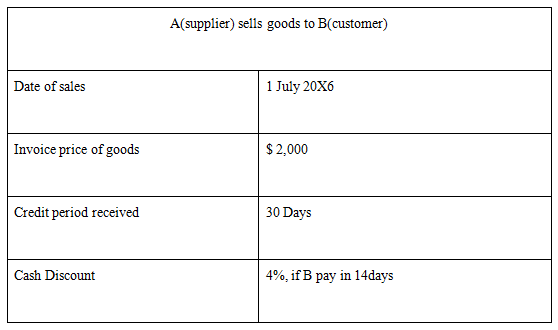

03、例題

接下來我們會分別展示站在銷售方A,和站在采購方B兩個不同的角度應該如何做會計處理:

Accounting for customer B:discount received

1. At 1 July 20x6. Initially record the purchase as follows 記錄采購:

Dr Purchases 2000

Cr Payable 2000

2. If subsequently take the discount(paid before 14 July 20x6)如果使用了現金折扣:

Dr Payable 2000

Cr Cash 1920 (2000-2000*4%)

Cr Discount received 80 (income) (2000*4%=80)

3、If subsequently not take (paid after 14 July 20x6)如果后續沒有使用現金折扣:

Dr Payable 2000

Cr Cash 2000

Accounting for supplier A:discount allowed

情景一:

1. At 1 July 20x6. If A expected the customer B will take the advantage of the early settlement discount銷售的時候預計客戶會使用現金折扣:

Dr Receivable 1920 (2000-2000*4%)

Cr Sales 1920

2. If subsequently take the discount (paid before 14 July 20x6)如果客戶后續確實使用了現金折扣

Dr Cash 1920

Cr Receivable 1920

3. If subsequently not take (paid after 14 July 20x6)如果后續客戶沒有使用現金折扣,這時候要調整我們之前記錄的銷售,之前認為銷售的金額是減去了折扣的,所以現在要調增:

Dr Cash 2000

Cr Receivable 1920

Cr Sales 80

情景二:

1. At 1 July 20x6. If A expected the customer B will NOT take the advantage of the early settlement discount 銷售的時候預計客戶不會使用折扣:

Dr Receivable 2000

Cr Sales 2000

2. If subsequently take the discount (paid before 14 July 20x6) 如果后續客戶使用了這個折扣,調整之前確認的銷售:

Dr Cash 1920

Dr Sale 80

Cr receivable 2000

3. If subsequently not take (paid after 14 July 20x6) 如果后續客戶沒有使用這個折扣:

Dr Cash 2000

Cr Receivable 2000

擴展閱讀

- 非居民企業和非居民個人可以享受國家支持疫情防控的稅收優惠政策? 2026-02-19

- 預繳企業所得稅時,沒有取得發票,可以扣除嗎? 2026-02-19

- 蘋果手機怎么調震動模式不要鈴聲 2023-08-17

- 貢獻邊際率公式是什么 2022-10-31

- 外幣報表折算差額怎么算? 2022-08-26

- 什么是介紹經紀人 2022-09-01

- 個人所得稅APP中匯算更正怎么辦理? 2026-02-08